Over the past decade, the BFSI (Banking, Financial Services, and Insurance) sector has invested heavily in digital transformation. According to Precedence Research, the global digital transformation market in BFSI reached $93.04 billion in 2024 and is expected to grow to $108.51 billion by 2025. Most financial institutions now have a solid digital foundation: modern core banking systems, mobile banking apps, e-payment gateways, and advanced data analytics platforms. Processes have been digitized, migrated to the cloud, and systems are interconnected.

But when it comes to implementing AI, the reality is: having a strong digital foundation does not mean an organization can master AI. So, what exactly is missing?

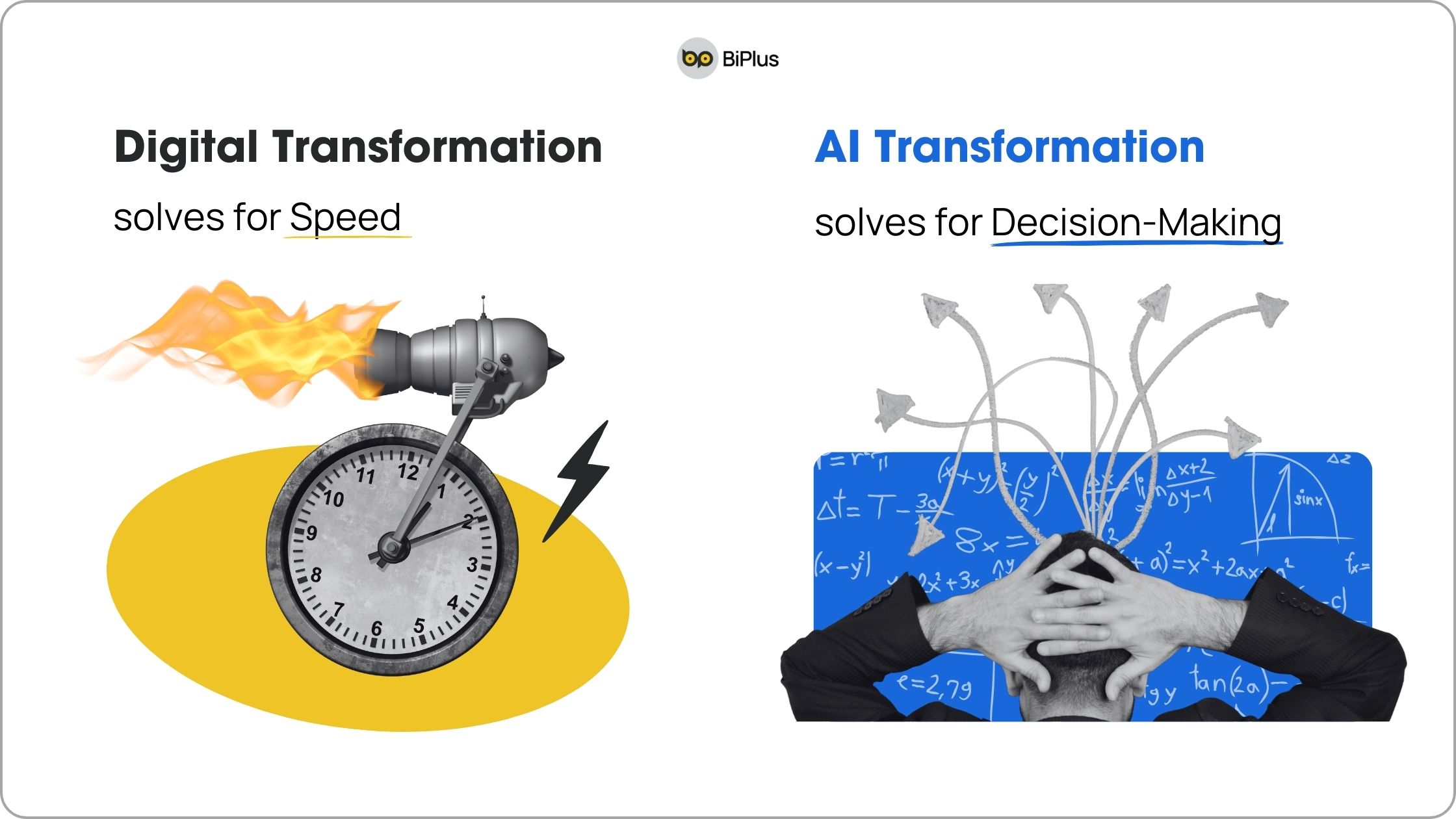

Digital Transformation Solves for Speed, AI Transformation Solves for Decision-Making

To understand the gap, we need to look at the essence of these two transformation stages.

Digital transformation focuses on digitizing what already exists. For example, a loan approval process that used to take five days with paper files now takes just two hours with digital systems. Customers who once had to visit a branch to check their balance can now do it on their phone in seconds. The nature of the work hasn't changed, approvers still review the same criteria, customers still perform the same actions. The only difference is that the environment has shifted from physical to digital.

AI transformation, on the other hand, changes the nature of decision-making. According to MJV Technology & Innovation, while digital transformation modernizes systems and processes to speed up operations, AI transformation aims to create smarter, more autonomous activities, predict trends, and enable entirely new business models.

A bank using AI for credit approval isn't just speeding up the old process. AI analyzes hundreds of variables that humans can't process simultaneously, detects hidden behavioral patterns, and adjusts evaluation criteria in real time based on market conditions. Decisions are no longer based on static checklists, they become dynamic and contextual.

This is where the real challenge begins.

BFSI Has Many Digital Tools but Lacks Digitized Workflows

A CTO at a major bank once shared: "We've implemented over 40 digital systems in the past eight years. But when we started using AI for fraud detection, I realized: no one really knows the full end-to-end fraud investigation process. Each branch does it differently. Key decisions are buried in emails or phone calls. Most of the know-how is in the heads of a few experts."

This is the reality for many BFSI organizations. They've invested in digital tools but haven't digitized their actual ways of working. Processes still rely heavily on personal experience, aren't documented, standardized, or centrally stored. Information about key decisions isn't systematically recorded.

During digital transformation, this wasn't a big issue because people still handled the work and could fill in the gaps themselves. For example, a seasoned credit officer knows what to ask, what to check, and how to spot red flags, even if these aren't written down.

But AI can't fill in the blanks like humans. AI needs clear, structured information about:

- Where does this task fit in the overall process?

- What were the previous decisions and why?

- Who is responsible for this outcome?

- Which steps require human review or approval?

If this information isn't digitized and systematically stored, AI remains a disconnected tool, unable to become an effective part of the organization's operations.

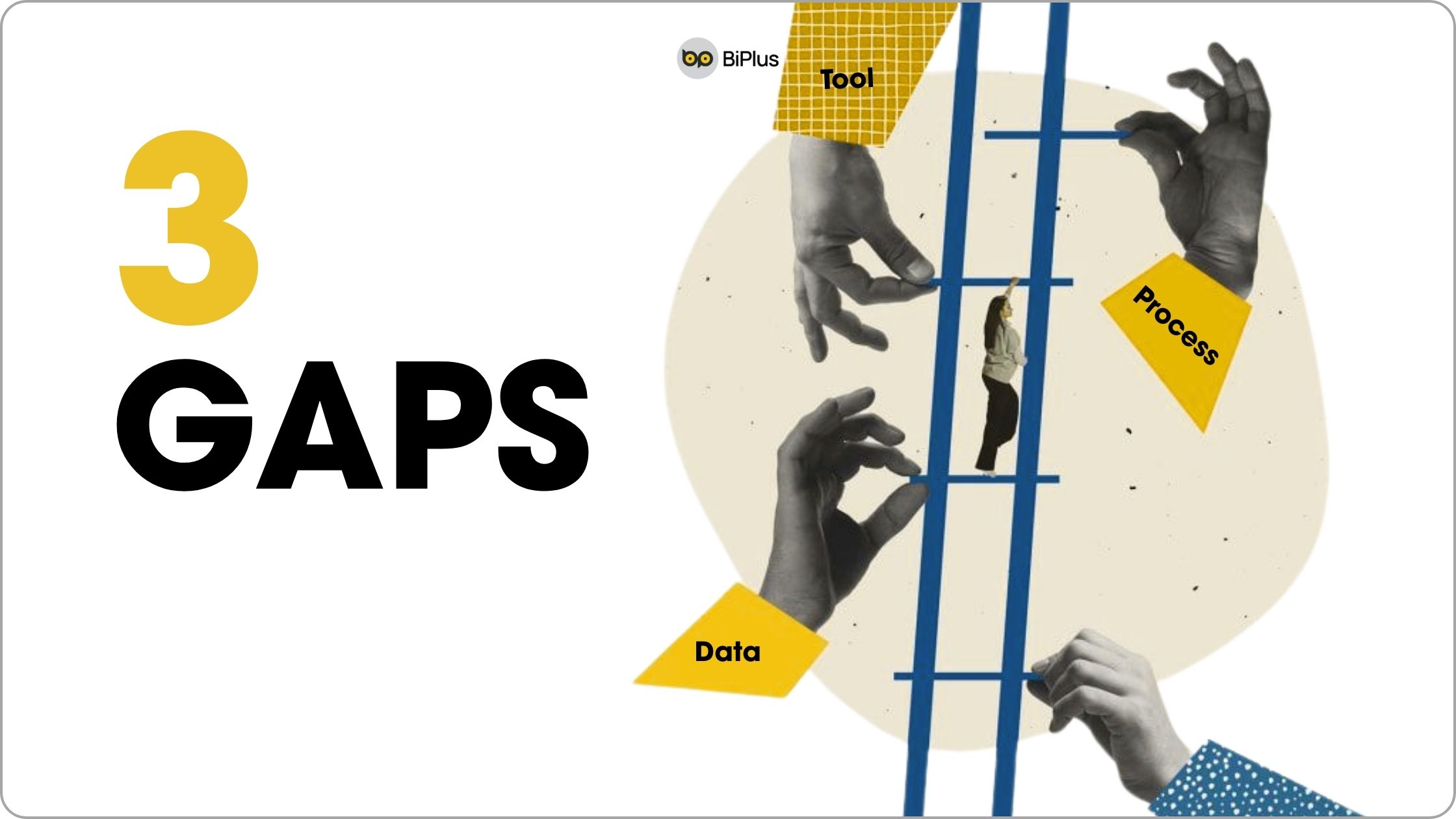

3 Gaps Preventing AI from Delivering Value After Digital Transformation in BFSI

After digital transformation, BFSI organizations have modern data platforms and digital tools. However, when deploying AI, three major gaps remain:

Gap 1: From Digital Data to Contextual Data

Digital transformation helps BFSI collect lots of data: transactions, customer profiles, interaction history, etc. But most of this data lacks context. For example, why was a decision made? What were the specific conditions at the time? How were exceptions handled?

An insurance company may have complete data on contracts and claims. But when training AI for risk assessment, they find the data doesn't explain why similar cases had different outcomes. The reason: exceptional decisions based on special contexts weren't recorded in the system, they only existed as personal experience.

AI needs data not just about "what happened" but also "why it happened."

Gap 2: From Digitized Processes to Observable Processes

Digital transformation digitizes process steps. But AI needs processes that are fully observable: what's happening, current status, who's responsible, where are the bottlenecks.

For example, a bank digitized its credit approval workflow. But in reality, many key tasks still happen outside the system, via email, meetings, or Slack. The system only reflects part of the reality. When deploying AI to optimize the process, they realize AI only sees a small piece of the whole picture.

Read more: Top 3 Reasons Why Teams Fail When "AI-izing" Their Workflows - In-depth analysis of risks when AI lacks process observability.

Gap 3: From Automation Tools to Systems with Clear Roles

Digital transformation enables many automation tools to support work. But AI needs to know who is responsible at each step. When AI makes a suggestion, who approves it? When AI detects an anomaly, who investigates? If AI makes a wrong decision, who is accountable?

In reality, many organizations deploy AI without clear accountability. IT manages the system, business uses the results, risk oversees but doesn't control the model. This makes AI a "gray area" of responsibility, posing risks when incidents occur.

Why AI Initiatives Struggle to Scale: Lessons from Practice

According to a McKinsey survey, 88% of organizations report using AI in at least one business function, but only 39% say AI impacts EBIT, and most of those report less than 5% of EBIT comes from AI.

The gap between "having AI" and "creating value from AI" largely comes from missing the link between digital platforms and AI: a structured system of work where AI can operate.

A securities company piloted AI investment advice in a small group with well-prepared data and tightly controlled processes. The results were impressive. But when scaling to 30 branches, they faced:

- Each branch recorded customer data differently

- Advisory processes weren't consistently documented

- No unified way to collect feedback on AI advice quality

- Branch managers didn't know how to monitor AI performance in their teams

These issues weren't due to weak AI. They resulted from lacking a unified system of work, something digital transformation doesn't require, but AI transformation demands.

The Missing Piece: System of Work

What BFSI needs to move from digital to AI transformation isn't more technology, but a System of Work - a way to organize work, roles, and knowledge so AI can be meaningfully integrated.

System of Work provides three things that digital platforms don't automatically create:

- Structure: Work is organized into observable processes, not just tacit knowledge

- Context: Decisions and reasons are recorded, not just outcomes

- Control: Roles and responsibilities are clear, so AI doesn't become a black box

When these three elements exist, AI is no longer a disconnected tool but becomes an intelligent layer embedded in how the organization operates.

AI-powered Systems of Work: Why AI only delivers value when embedded in how your business operates? - Read more about this concept.

What Leading Organizations Do Differently

According to McKinsey, only 6% of organizations, those with high performance, are capturing outsized value through systematic AI deployment. The difference isn't better AI technology or bigger budgets.

They don't rush to deploy AI after digital transformation. Instead, they spend time to:

- Standardize ways of working across the organization

- Systematically document processes

- Build a culture of recording knowledge and context

- Define clear roles and responsibilities before automating

A regional bank spent 18 months building a System of Work before deploying AI for credit analysis. During that time, they didn't write a single line of AI code. Instead, they:

- Unified credit approval processes across all branches

- Documented exceptional decisions and reasons

- Created mechanisms for experts to record knowledge in the system

- Clearly defined where AI supports and where humans decide

When they finally deployed AI, they scaled in three months instead of 18 like competitors. Not because their AI was better, but because their foundation was stronger.

Questions BFSI Leaders Should Ask Themselves

Instead of asking "Have we completed digital transformation?", BFSI leaders should ask:

- Are our core processes consistently documented across the organization?

- When a key decision is made, is the context and reason recorded?

- If an expert leaves, does their knowledge leave with them?

- Can we observe where work is happening and its status?

- When deploying AI, do we know who is responsible for each type of decision?

If the answer is "not yet" or "not sure," that's the missing piece.

Need a Robust System of Work to Step into AI Transformation?

BiPlus is Atlassian's partner in Vietnam, supporting many BFSI organizations to standardize workflows and project management on Jira and Confluence; redesign collaboration between business, technology, risk, and compliance teams to be AI-ready; and build AI use cases closely tied to real operations such as credit approval, risk management, fraud detection, and customer service.

Instead of deploying scattered tools, BiPlus helps organizations build a Teamwork Collection as a unified AI-powered System of Work for the entire organization.

Teamwork Collection is a modern solution for building a unified work management system, connecting people, processes, and tools in a seamless ecosystem. Teamwork Collection supports your teams to:

- Focus on work management, cross-department collaboration, and knowledge management, enabling transparent, accountable, and measurable teamwork.

- Deeply integrate with AI and data to support faster decision-making, reduce manual work, and ensure enterprise-level compliance and security.

- Suit BFSI organizations looking to boost productivity, standardize processes, and build a flexible digital foundation for long-term growth.

If you want to leverage AI for value creation and risk control, contact BiPlus to discuss your roadmap for building a System of Work and deploying Teamwork Collection for your BFSI organization.

Conclusion: The Missing Piece Isn't Technology

BFSI organizations have invested billions in digital transformation to build a solid digital foundation. But that's only the necessary condition, not enough for successful AI transformation.

What's missing isn't AI technology, but the System of Work, how work is organized, roles are defined, and knowledge is managed so AI can operate in a controlled, transparent way across the organization.

From our experience working with financial institutions in Vietnam, BiPlus has seen that those who successfully move from digital to AI transformation always start by investing in building a System of Work. They don't rush into AI, but focus on standardizing processes, clarifying responsibilities, and ensuring all data and decisions are tightly controlled. Only then can AI deliver real value and minimize risks.

In 2026, the difference between organizations that succeed with AI and those that fail won't be who has the most advanced technology, but who has built a robust enough System of Work for AI to truly create value for the business.

If you're interested in digital transformation, contact BiPlus to schedule a 1:1 consultation on building your System of Work and deploying Teamwork Collection tailored to your organization's needs.